Universal Credit is now the main social security that people on benefits claim from the Department for Work and Pensions (DWP). At the minute, a lot of people want to know how much is Universal Credit going up by.

However, more importantly what is it? How do you claim it? How much do you get? Where did Universal Credit come from? And what are the problems with it you’re not hearing about? Here, the Canary explains all.

What is Universal Credit?

It’s the main benefit that people can claim from the Department for Work and Pensions (DWP) now. Universal Credit has been replacing six old-style benefits like Employment and Support Allowance (ESA) and Jobseeker’s Allowance (JSA) since 2013. The DWP has gradually rolled it out across the UK. More and more people have been claiming it as time has gone on.

The DWP designed Universal Credit so that all types of claimants are entitled to it. Generally, it’s for people over the age of 18. This includes jobseekers, chronically ill and disabled people, and people who have caring responsibilities. They would have previously claimed ESA or JSA. Also, people who don’t earn much money because of their job can claim it as well. They would have previously claimed Working Tax Credits.

How much is Universal Credit?

How much Universal Credit will I get?

That really depends on your circumstances. The DWP has made it quite complicated in terms of different payment rates. It breaks the benefit down into different parts (elements). However, the basic amounts (“standard allowance“) Universal Credit gives you are as follows.

If you’re aged under 25, from 1 April 2023 you’ll get:

- £292.11 a month if you’re single.

- £458.51 a month for couples (“joint claimants”).

If you’re aged over 25, you’ll get:

- £368.74 a month if you’re single.

- £578.82 a month for couples.

Then, you may be entitled to other parts of Universal Credit.

Kids, health and disability, and housing

If you have children, the Department for Work and Pensions (DWP) might give you more money to help you with their costs. However, it will only pay for up to two children. This is called the two-child limit. Under Universal Credit, you might get:

- £315 a month for your first or only child. However, they need to have been born before 6 April 2017.

- £269.58 a month for a second child, or for one child born after 6 April 2017.

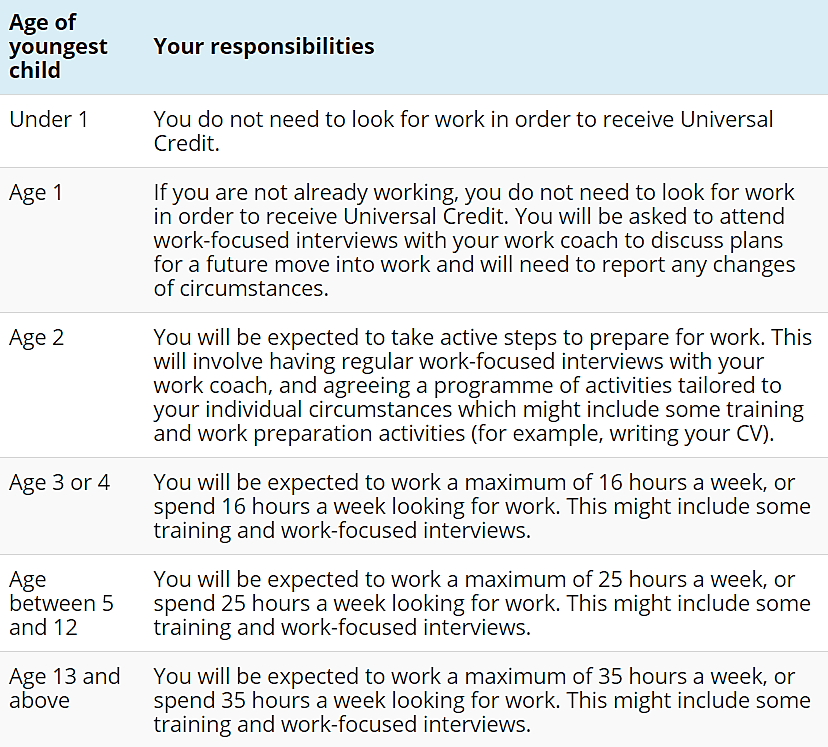

If you have a child/children, the DWP might say you should be working when you’re not, or that you’re not working enough. It will then force you to do certain things to get Universal Credit. What these are depends on the age of your child:

If you are a chronically ill or disabled person, you might get the Limited Capability for Work or Work-Related Activity (LCWRA) element. This means the DWP shouldn’t make you do anything regarding getting a job. It will give you:

However, to get this, you have to pass an assessment. There’s more on that further down this page.

If you’re an unpaid carer, the DWP may give you:

- £185.86 a month.

The DWP might also give you the housing element. How much it will give you depends on a lot of things. So, it’s best to read the DWP’s guide on this here.

Working, and work-related groups

You can work and claim Universal Credit as well.

How much can you earn and still get Universal Credit?

This depends on your circumstances. It also depends on whether you are part of a couple, and what the other person’s circumstances are. However, as a rough guide – if you have a child, or you have Limited Capability For Work, the Department for Work and Pensions (DWP) will give you a Work Allowance. This is an amount you can earn before the DWP starts reducing your Universal Credit payments. The DWP will give you a Work Allowance of:

- £379 a month if it also gives you the housing element.

- £631 a month if it doesn’t give you the housing element.

After these amounts, the DWP starts deducting money off your Universal Credit. For every pound you earn, it takes 55p back from your benefits payment.

If you’re self-employed, the DWP also has rules around how much it thinks you should be earning. This is called the Minimum Income Floor. The DWP expects all self-employed claimants who can work full time to be earning the same as someone who does 35 hours a week at a minimum wage job. If the DWP doesn’t expect you to work full time, then the Minimum Income Floor is based on the number of hours it does expect you to do.

How many hours can you work on Universal Credit?

If you’re just working, and not claiming disability or health elements, then the Department for Work and Pensions (DWP) doesn’t base your payments on how many hours you work. It bases them on how much you earn.

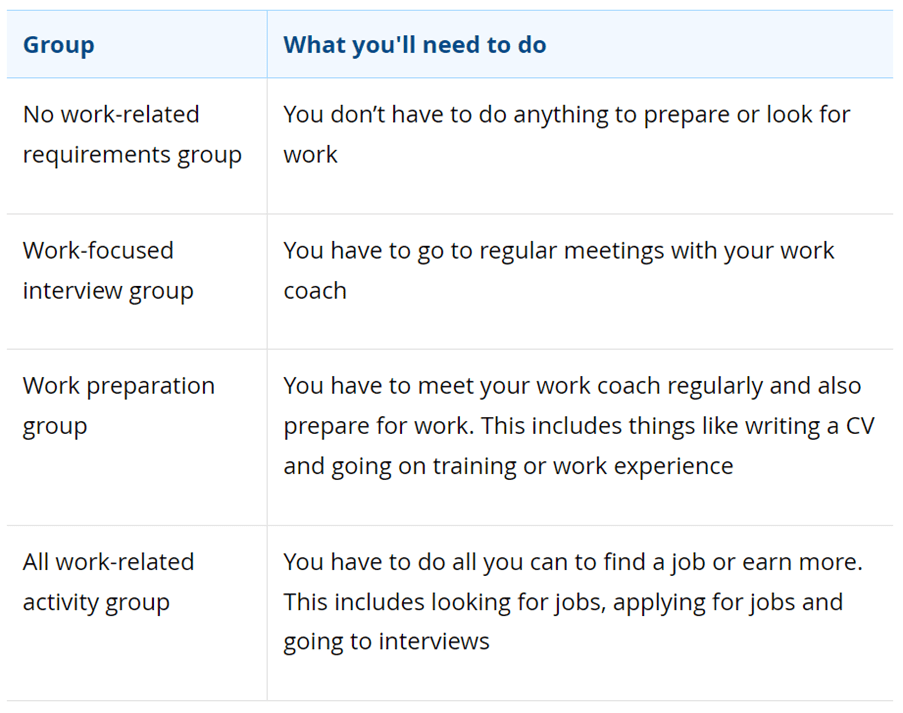

Once the DWP has decided what you’re entitled to, it puts you into a group. These are based on what it expects you to do regarding work. The DWP makes this decision based on your circumstances. For example, if it says you have LCWRA then it will put you in the “no work-related requirements group”:

How much is Universal Credit going up by in April 2024?

The Department for Work and Pensions (DWP) increased Universal Credit by 10.1% from 1 April 2023. However, benefit claimants didn’t actually see an increase in April, overall. In reality, the DWP took people’s benefits back up to the rate they were at in April 2022. This is because the rising cost of everything (‘inflation’) was been more than the DWP’s 10.1% increase. This is called a ‘real-terms cut’.

So, while the DWP may be giving claimants more money, it’s not giving them enough to make up for the fact everything is more expensive now.

New Universal Credit rates April 2024

From April 2024, the DWP will put Universal Credit up again. The rates will change to the following:

| Standard allowance | ||

| Single under 25 | 292.11 | 311.68 |

| Single 25 or over | 368.74 | 393.45 |

| Couple – joint claimants both under 25 | 458.51 | 489.23 |

| Couple – joint claimants, one or both 25 or over | 578.82 | 617.60 |

| Child amounts | ||

| First child (born prior to 6 April 2017) | 315.00 | 333.33 |

| First child (born on or after 6 April 2017)/ second child and subsequent child (where an exception or transitional provision applies) | 269.58 | 287.92 |

| Disabled child additions | ||

| Lower rate addition | 146.31 | 156.11 |

| Higher rate addition | 456.89 | 487.58 |

| Limited capability for work amount | 146.31 | 156.11 |

| Limited capability for work and work-related activity amount | 390.06 | 416.19 |

| Carer amount | 185.86 | 198.31 |

| Childcare costs amount | ||

| Maximum for one child | 950.92 | 1014.63 |

| Maximum for two or more children | 1630.15 | 1739.37 |

| Non-dependants’ housing cost contributions | 85.73 | 91.47 |

| Work allowances | ||

| Higher work allowance (no housing amount) one or more dependent children or limited capability for work | 631.00 | 673.00 |

| Lower work allowance – one or more dependent children or limited capability for work | 379.00 | 404.00 |

However, most people will still be worse off because of inflation. For example, think tank the New Economics Foundation says that:

- An out-of-work single person over 25 on Universal Credit would be £670 a year worse off than in April 2023.

- A a lone parent with one child would be £350 worse off.

- A couple over 25 with two children would only be £35 a year better off.

How to apply for Universal Credit

You can make an application here:

If you are a disabled or chronically ill person, the Department for Work and Pensions (DWP) will make you wait three months before it will pay you extra money for your condition. It may make you do a Work Capability Assessment (WCA). This is where the DWP will assess whether you’re entitled to extra financial support.

You need to prepare for the WCA. Make sure you have as much evidence from doctors about your condition as you can get. Be prepared to explain to, and show, the DWP why you cannot do much work, or work at all. And if the department says you’re not entitled to extra money, always challenge this with a Mandatory Reconsideration – if you have the capacity to.

More advice on the WCA is available here.

Universal Credit login

If you already claim Universal Credit, or have done recently, you can access your account here:

Does PIP affect Universal Credit?

No, Personal Independence Payment (PIP) does not affect Universal Credit at all. Its predecessor – Disability Living Allowance (DLA) – doesn’t, either.

PIP is not a means-tested benefit. That is, it doesn’t matter if you’re rich, poor, or just ‘doing OK’. The DWP will give you PIP if it says you’re chronically ill or disabled enough to get it. So, because PIP is not means tested, it has nothing to do with Universal Credit.

Where did Universal Credit come from?

It was the idea of the Conservative Party – specifically Iain Duncan Smith MP and his think tank the Centre for Social Justice.

When the Tories were in opposition in the noughties, then-leader David Cameron asked Duncan Smith to come up with an idea to change the benefits system. He wanted to make the Department for Work and Pensions (DWP) cost less for the government, and also to stop poor people claiming benefits.

The Tories believe that poverty is partly the fault of poor people, due to things like education and addiction. So, Duncan Smith designed Universal Credit with the belief that people could get a job to get out of poverty. However, he also thought that Universal Credit should use punishments like sanctions and cutting people’s money to try to force them to stop claiming benefits and get into work.

Is poverty people’s fault?

So, the Tories think that if you’re poor, it’s probably your own fault – and that work is the best thing you can do to not be poor.

However, a lot of evidence shows this is not true. For example, bosses have been paying people really low wages for years. People are not earning as much (in real terms) now as they were in 2008. This is also the Conservative Party’s fault, as it’s been in government for most of that time.

For example, it has never set the rate of the national minimum wage at the level of the so-called “Real Living Wage“. So, bosses have always been able to get away with paying people really low wages.

What are the problems with it?

Universal Credit has been controversial since it was launched. Here are some of its biggest scandals:

- The Department for Work and Pensions (DWP) colluded with Sainsbury’s to spy on benefit claimants when they were shopping.

- Its two-child limit (which also applies to Child Tax Credit) has been extremely controversial. For example, in a court case on it one judge called the limit “perverse”. It has increased child poverty. Then, there’s the so-called ‘rape clause‘. This where women have to prove they’ve been raped to get an exception to the two-child limit. Plus, Canary research shows it may well have caused more women to have abortions, and birth rates among the poorest people to fall.

- Severely disabled people had to repeatedly take the DWP to court. This was over the department cutting their benefits when they moved from ESA to Universal Credit. There have been numerous other Universal Credit court cases, too.

- The DWP’s use of sanctions (where it stops people’s money) under Universal Credit has been heavily criticised. When claimants challenge a sanction, the DWP is often found to have wrongly stopped their money.

Canary thoughts on Universal Credit

Victorian thinking

Steve Topple previously wrote for the Canary:

What drove all this thinking seems to me to be Victorian-era, Christian fundamentalist values. Essentially, the notion of the ‘deserving’ and ‘undeserving’ poor.

All of the contemporaneous… work pushes the idea that it’s poor people’s behaviours and attitudes that must change, not capitalism. It, of course, ignores the fact that its five “pathways to poverty” are all symptoms of capitalism itself; not of people’s bad behaviour.

But… [its architects] couldn’t acknowledge this, as it would naturally render them, and the capitalist-driven Conservative Party, null and void.

So essentially, their thinking was if you’re poor, you made yourself that way; shown in the “pathways to poverty”. To stop poor people being stupid and making themselves destitute, the government needed to shake up the benefits system; to nudge everyone possible into work, and those in work into more work; making welfare reliance impossible. And anyone left? It’s their own, stupid fault.

So to do this, the… [Tories] created Universal Credit.

But it would also put all those unwilling to help themselves out of poverty and welfare into one place. Sick, disabled, unemployed and low earning people would no longer be different, distinct benefit groups. They would become one, homogeneous ‘underclass’ of people. And, as the… [Tories’] early thinking shows, the state would give minimal support to these people. Instead, charities and communities should carry the burden of this workless/underemployed group.

A dystopian nightmare

Universal Credit is the perfect vehicle for the 21st-century ‘Victorian mindset’. It sanctions low paid workers who aren’t doing enough to get more work; penalises lone parents; cuts free school meals; reduces support for disabled people with severe impairments. And, by design, it encourages people’s reliance on charity – note the rise of food banks.

Universal Credit’s history shows why… it cannot be ‘fixed’.

Its architects designed it to marginalise whole sections of society; to create a dystopian world where an underclass of people exists on its fringes.

Couple this with the government cutting public services left, right and centre; homelessness rocketing; social housing decimated – and we are seeing a nightmarish vision, once reserved for science fiction, becoming a reality. Universal Credit needs to be stopped and scrapped.

What can you do to change Universal Credit for the better?

You can get involved with grassroots campaign groups to protest and take action over Universal Credit. These include:

- Disabled People Against Cuts (DPAC).

- Unite Community.

- The Disability Union.

- The Chronic Collaboration.

Got a story about your experience of Universal Credit? Email us via editors(at)thecanary.co

Featured image via the Canary and Wikimedia

{kind=link}